A capital commitment is the total amount an investor agrees to contribute to a private equity or venture capital fund over time. Rather than paying the full amount upfront, limited partners (LPs) fund their commitments through capital calls issued during the investment period. This article explains how capital commitments work, outlines the key terms, and explores how LPs manage timing, risks, and legal obligations.

Key Takeaways

- Capital commitment is a binding legal obligation to invest a specific amount in a fund over time, with capital drawn through formal capital call notices

- The commitment-drawdown model allows funds to access capital precisely when investment opportunities arise while investors earn returns on uncalled capital

- Commitment periods typically span 3-5 years for new investments, followed by additional years for follow-on investments and expenses

- Default remedies for missed capital calls include financial penalties, forced sale of fund interests at 50% discounts, and loss of voting rights

- Subscription facilities have transformed capital call patterns, allowing funds to delay LP capital calls while maintaining deal execution capability

What Is Capital Commitment and How Does It Work?

Capital commitment forms the operational backbone of private market investing, creating a contractual framework that governs how and when investment capital flows from limited partners to general partners throughout a fund's lifecycle. This sophisticated system balances efficient capital deployment with investor protection while enabling the $13 trillion private markets ecosystem to function effectively.

When investors commit capital to a private equity or venture capital fund, they sign a Limited Partnership Agreement (LPA) that creates a legally enforceable obligation to provide their committed amount when called upon by the fund manager. This commitment represents the maximum amount an investor agrees to invest over the fund's investment period, though the actual amount called may be less if the fund doesn't identify sufficient attractive investment opportunities.

The commitment structure distinguishes private markets from traditional investments through three distinct capital stages:

Committed Capital: The total amount investors pledge to contribute over the fund's life, serving as the basis for management fee calculations and fund size reporting. This represents a contractual promise rather than actual cash transfer.

Called Capital: The portion of committed capital that has been formally requested by the general partner through capital call notices. This includes amounts for portfolio investments, management fees, and fund expenses.

Invested Capital: The specific portion of called capital deployed into portfolio companies, excluding fees and expenses. This forms the basis for performance calculations like Multiple on Invested Capital (MOIC).

The Capital Call Process

The capital call process represents the mechanism through which committed capital transforms into actual investments. This systematic approach ensures proper governance while maintaining the flexibility needed for opportunistic investing.

Step 1: Investment Opportunity Identification

Capital calls begin when fund managers identify compelling investment opportunities that align with the fund's strategy. The investment committee must rapidly assess opportunities against fund criteria, projected returns, and portfolio construction parameters.

Step 2: Capital Requirements Calculation

Fund managers must calculate total capital needs beyond the headline investment amount, including:

- Core investment amount for equity purchase

- Transaction costs including legal fees, due diligence expenses, and advisory fees

- Working capital buffer for portfolio company operations

- Management fees and partnership expenses

- Reserve allocations for anticipated follow-on investments

Step 3: Limited Partner Allocation Determination

Each limited partner's share is calculated based on their pro rata commitment percentage, adjusted for any side letter provisions or previous capital calls. Most funds utilize pro rata systems where all LPs contribute the same percentage of their committed capital regardless of absolute amounts.

Step 4: Formal Notice Issuance

The general partner issues capital call notices typically providing 10-14 days for payment, including:

- Specific amount being called from each LP

- Percentage of total commitment represented

- Purpose of the capital call with investment details

- Payment deadline and wire transfer instructions

- Total capital called to date and remaining unfunded commitment

- Default consequences for non-payment

Step 5: Capital Transfer and Deployment

Limited partners wire funds according to instructions, with the GP tracking receipt and deploying capital according to the investment plan. Modern funds often use capital call facilities to bridge timing gaps between opportunity identification and LP funding.

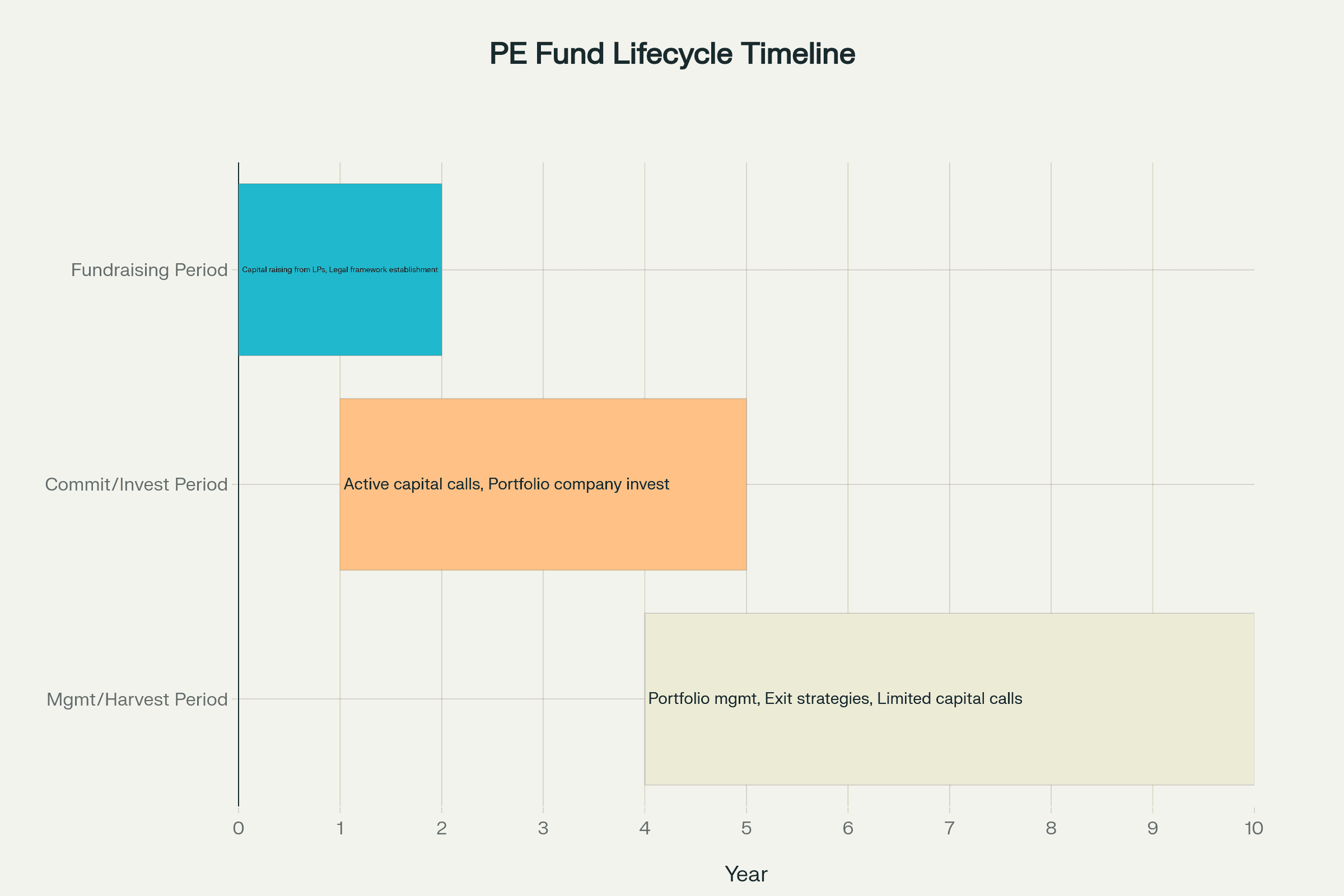

Commitment Period Timeline

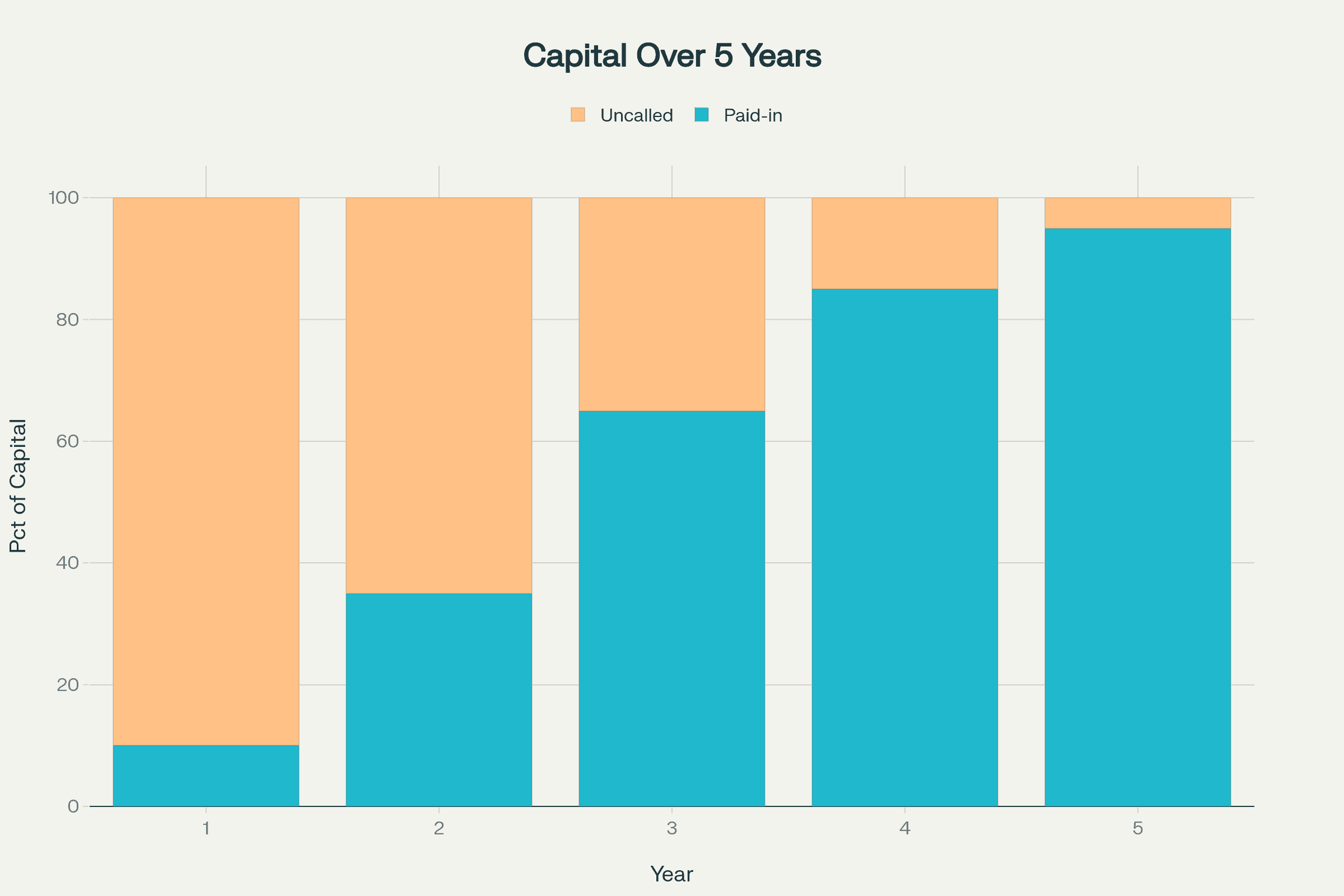

The commitment period defines when general partners can call capital for new investments, creating a structured timeline for fund deployment. This period, also known as the investment period, typically spans 3-5 years from the fund's final closing, though specific durations vary by strategy.

During the commitment period, funds actively source and execute new investments with distinct patterns by fund type:

Years 1-2: Accelerated deployment phase with 40-60% of commitments typically called as funds establish initial portfolio positions. Private equity funds may make 3-5 platform investments while venture funds seed 15-25 companies.

Years 3-5: Continued deployment at measured pace, balancing new investments with reserve management for follow-ons. Capital calls moderate as funds approach full deployment.

Post-Commitment Period: After the investment period expires, capital calls are restricted to:

- Follow-on investments in existing portfolio companies

- Pre-agreed investments committed during the investment period

- Management fees calculated on invested capital rather than commitments

- Fund expenses and working capital needs

This structured approach provides predictability for investor liquidity planning while ensuring fund managers maintain flexibility to capitalize on time-sensitive opportunities throughout the investment lifecycle.

Capital Commitment in Private Equity vs Venture Capital

While both private equity and venture capital utilize capital commitment structures, their deployment patterns, timing, and risk management approaches differ significantly based on underlying investment strategies and portfolio construction methodologies.

Private Equity Commitment Patterns

Private equity funds focus on established businesses with predictable cash flows, typically deploying capital in larger, concentrated investments. A buyout fund might invest $100 million or more per transaction, acquiring controlling stakes in 10-15 companies throughout the commitment period. This concentrated approach creates distinct commitment characteristics:

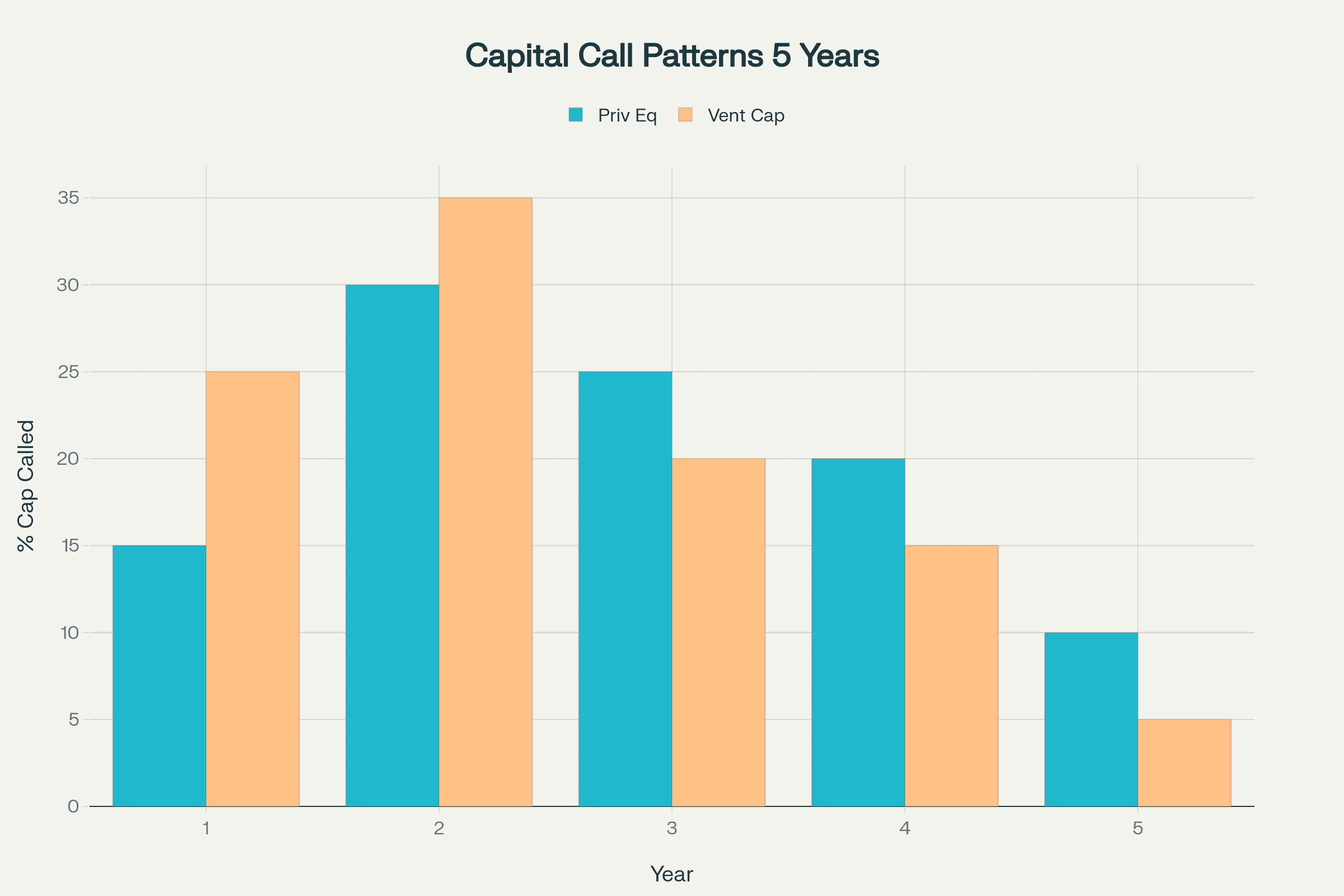

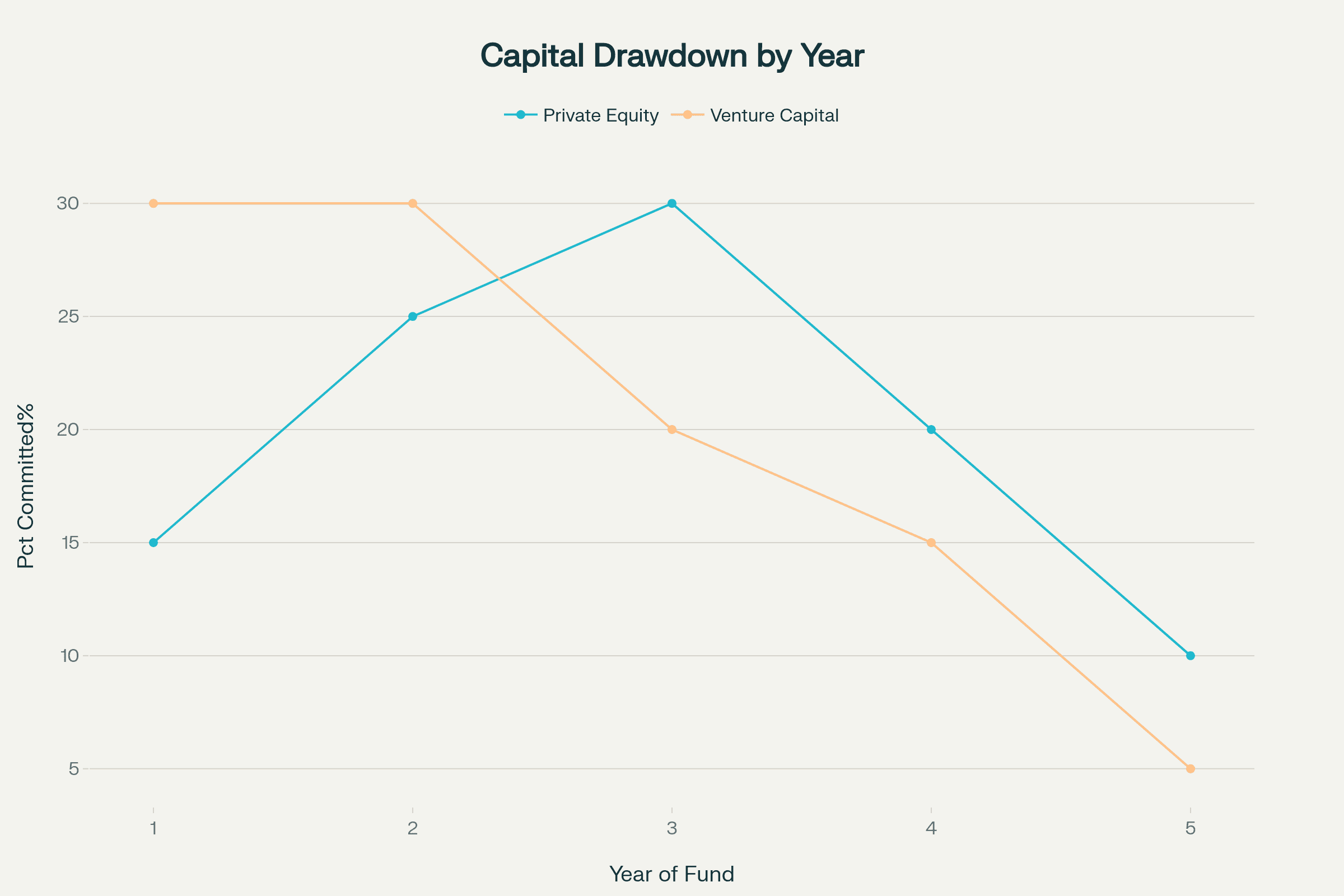

Deployment Velocity: PE funds typically call 60-80% of committed capital within the first three years, reflecting the need for substantial upfront capital to complete leveraged buyouts. The Yale model suggests 15% deployment in year one and 25% in year two, with continued aggressive deployment through year four.

Capital Call Predictability: Buyout funds provide more predictable capital call schedules due to lengthy due diligence periods and structured acquisition processes. Limited partners often receive informal advance notice weeks before formal capital calls, enabling sophisticated liquidity management.

Subscription Facility Usage: Private equity funds extensively utilize capital call facilities to enhance returns and operational flexibility. These credit lines, secured by unfunded LP commitments, allow funds to complete acquisitions immediately while delaying LP capital calls by 6-12 months. This practice has become standard, with facilities often sized at 15-20% of total commitments.

Reserve Requirements: PE funds typically maintain lower reserves relative to venture capital, as follow-on investments in mature companies are more predictable. Reserves of 10-20% of initial investment amounts suffice for add-on acquisitions and portfolio company support.

Venture Capital Commitment Patterns

Venture capital commitments follow fundamentally different patterns driven by the staged nature of startup investing and higher portfolio company mortality rates. VC funds construct portfolios of 25-50 companies, with initial investments representing small percentages of total fund size.

Gradual Deployment Curve: Venture funds typically call only 25-30% of commitments in the first two years, reserving substantial capital for follow-on rounds. Early-stage funds may take 5-6 years to reach 50% deployment, reflecting the need to support portfolio companies through multiple funding rounds.

Unpredictable Call Timing: The success-based nature of follow-on investing creates irregular capital call patterns. A breakout portfolio company raising successive rounds can trigger unexpected capital calls, while failed investments reduce future capital needs. This unpredictability requires LPs to maintain higher liquidity buffers.

Extended Investment Periods: Many venture funds negotiate longer investment periods of 4-6 years to accommodate the extended development timelines of early-stage companies. Some agreements allow investment period extensions if specified percentages remain undeployed, providing flexibility for patient capital deployment.

Reserve Strategy Complexity: Venture funds must balance competing demands for capital between new investments and follow-on support for existing portfolio companies. Industry practice suggests reserving 50-100% of initial investment amounts for follow-ons, though actual needs vary dramatically based on portfolio performance. This creates modeling challenges for both GPs and LPs.

Commitment Risk Profiles

The structural differences between PE and venture capital create distinct risk profiles for limited partner commitments:

Concentration Risk: Private equity's larger, concentrated investments create binary outcome risks where single investment failures can materially impact fund returns. Venture capital's broader portfolios provide diversification but require at least one significant winner to drive fund-level returns.

J-Curve Variations: PE funds typically exhibit shallower J-curves with faster return of capital through dividend recapitalizations and strategic exits. Venture J-curves run deeper and longer, with returns concentrated in later years as successful companies achieve liquidity events.

Capital Efficiency: Private equity's use of leverage and operational improvements can generate returns with less equity capital at risk. Venture capital relies purely on equity appreciation, requiring larger multiples on invested capital to achieve similar fund-level returns.

Common Questions About Capital Commitment

What happens if an investor can't meet a capital call?

Defaulting on capital calls triggers severe consequences outlined in the Limited Partnership Agreement. The LPA typically provides general partners with comprehensive remedies including punitive interest rates of 10% or higher on unfunded amounts, reduction of the defaulting investor's capital account by 50-100%, and forced sale of their entire fund interest at significant discounts often around 50% of net asset value. Defaulting investors also lose voting rights, advisory committee participation, and any negotiated benefits under side letters. To address shortfalls, GPs can implement overcall provisions allowing non-defaulting investors to cover gaps, though these are typically capped at 50% of original commitments to prevent excessive burden.

Can investors reduce or cancel their capital commitments?

Capital commitments are legally binding obligations that generally cannot be reduced or cancelled unilaterally once made. However, certain exceptional circumstances may allow modifications. Some LPAs include performance-based cancellation rights if fund returns fall below specified thresholds, such as 20% annual losses. Regulatory restrictions or legal impediments may excuse investors from funding obligations if properly documented. Rather than cancellation, investors typically pursue secondary market sales of their fund interests, though these often occur at discounts to net asset value and require GP consent.

How do funds handle uncalled capital commitments?

General partners must carefully manage uncalled commitments through sophisticated cash flow forecasting and capital deployment planning. Most funds maintain capital call lines of credit to bridge timing gaps between investment identification and LP funding, enabling immediate deal execution. From the investor perspective, uncalled commitments should be managed through time-based segmentation: near-term calls (6-12 months) held in cash or money market funds, medium-term (1-2 years) in investment-grade fixed income, and longer-term in public equities. Many LPAs allow GPs to release excess commitments they don't expect to call, reducing LP obligations and freeing capital for other uses.

What's the difference between committed capital and invested capital?

Committed capital represents the total amount investors pledge to contribute over the fund's life, serving as a contractual obligation and the basis for management fee calculations. Invested capital represents actual cash deployed into portfolio companies, excluding management fees and expenses. This distinction critically impacts performance measurement: IRR calculations use called capital cash flows while MOIC uses invested capital as the denominator. The difference means effective fee rates calculated against invested capital exceed stated percentages, and investors must track both metrics for accurate portfolio management.

How do commitment facilities affect LP capital calls?

Subscription facilities fundamentally alter traditional capital call patterns by allowing funds to borrow against uncalled LP commitments. These revolving credit lines, typically sized at 15-20% of fund commitments, enable GPs to invest immediately while delaying LP capital calls by 6-12 months. Benefits include reduced call frequency through grouped investments, enhanced deal execution speed, and improved LP liquidity management. However, facilities artificially boost IRR by 1-3% annually while reducing absolute returns due to interest costs. Industry best practices now recommend reporting both levered and unlevered performance metrics for transparency.

Conclusion

Capital commitment structures will continue evolving as private markets expand their role in global capital allocation. Success in this environment requires sophisticated understanding of commitment mechanics, robust operational systems for tracking obligations across multiple funds, and disciplined portfolio construction approaches. The increasing prevalence of subscription facilities, growing secondary markets, and evolving fund structures demand that both general partners and limited partners continuously refine their approach to capital commitment management. As the industry matures, maintaining transparency in capital processes while ensuring proper alignment between GP and LP interests remains essential for sustainable growth and value creation in private markets.