Capital calls are how private equity and venture capital funds draw down committed capital from their investors. When a fund identifies an investment or needs to cover expenses, it issues a capital call—typically with 10 to 30 days’ notice. In this guide, you’ll learn how capital calls work, when they happen, the risks for LPs, and best practices for managing your commitments effectively.

KEY TAKEAWAYS

- Capital calls are formal requests from fund managers to limited partners (LPs) to transfer a portion of their committed capital to the fund for specific investments or expenses

- Investors typically have 10-30 days to respond to a capital call, with penalties ranging from interest charges to forfeiture of partnership interests for non-payment

- Capital calls usually represent 10-25% of an investor's total commitment per call, with multiple calls occurring throughout the fund's investment period (typically 3-5 years)

- Fund managers must follow strict procedures outlined in the Limited Partnership Agreement (LPA) when issuing capital calls, including providing detailed notices and justifications

- Understanding capital call mechanics is crucial for both general partners (GPs) managing liquidity and limited partners planning their cash flow requirements

What Are Capital Calls and How Do They Work?

A capital call, also known as a "drawdown" or "capital commitment call," is a legally binding request made by a private equity or venture capital fund's general partner (GP) to its limited partners (LPs) to contribute a portion of their committed capital. This mechanism allows funds to draw capital from investors only when needed for investments, operational expenses, or management fees, rather than requiring the full commitment upfront.

The capital call process represents a fundamental aspect of how alternative investment funds operate. Unlike mutual funds or ETFs where investors contribute their full investment amount immediately, private equity and venture capital funds use a commitment-and-call structure that optimizes capital efficiency for both managers and investors.

When an investor commits to a private equity fund, they're essentially promising to provide a specific amount of capital over the fund's life, typically 10-12 years. The fund manager then "calls" this capital in increments as investment opportunities arise, usually during the first 3-5 years (the "investment period"). This staged approach allows investors to maintain liquidity with their uncalled capital while giving fund managers the flexibility to deploy capital opportunistically.

The Capital Call Process

The capital call process follows a structured sequence designed to ensure transparency and compliance:

-

Investment Opportunity Identification: The GP identifies an investment opportunity or operational need requiring capital. This includes thorough due diligence and investment committee approval.

-

Call Notice Preparation: The fund administrator prepares a formal capital call notice following ILPA (Institutional Limited Partners Association) best practices, detailing:

- Amount being called (absolute and percentage of commitment)

- Purpose of the call with transaction rationale

- Due date for funds (typically 10-30 days from notice)

- Wire transfer instructions with security protocols

- Consequences of non-payment as specified in the LPA

- Reference to relevant LPA sections

-

Notice Distribution: LPs receive the call notice via multiple channels - typically email, secure portals, and registered mail - with advance notice periods specified in the LPA.

-

Capital Transfer: LPs wire their proportionate share of the called capital by the specified deadline. Many sophisticated LPs utilize capital call lines of credit to bridge timing gaps.

-

Investment Execution: The GP deploys the collected capital according to the stated purpose, maintaining strict segregation of fund assets.

-

Reporting: The fund provides updates on capital deployment, investment performance, and updated commitment balances through quarterly reports and LP portals.

Types of Capital Calls

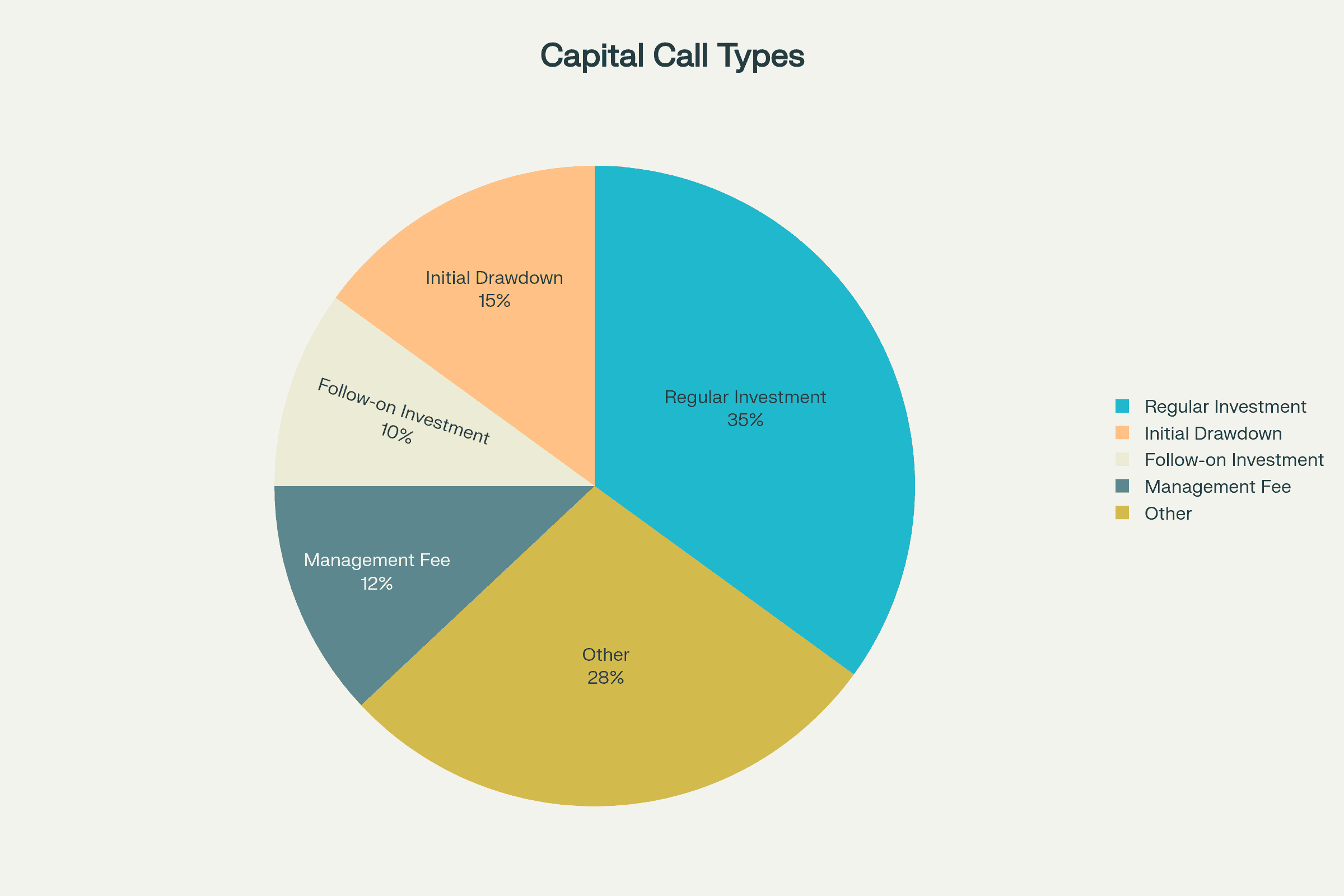

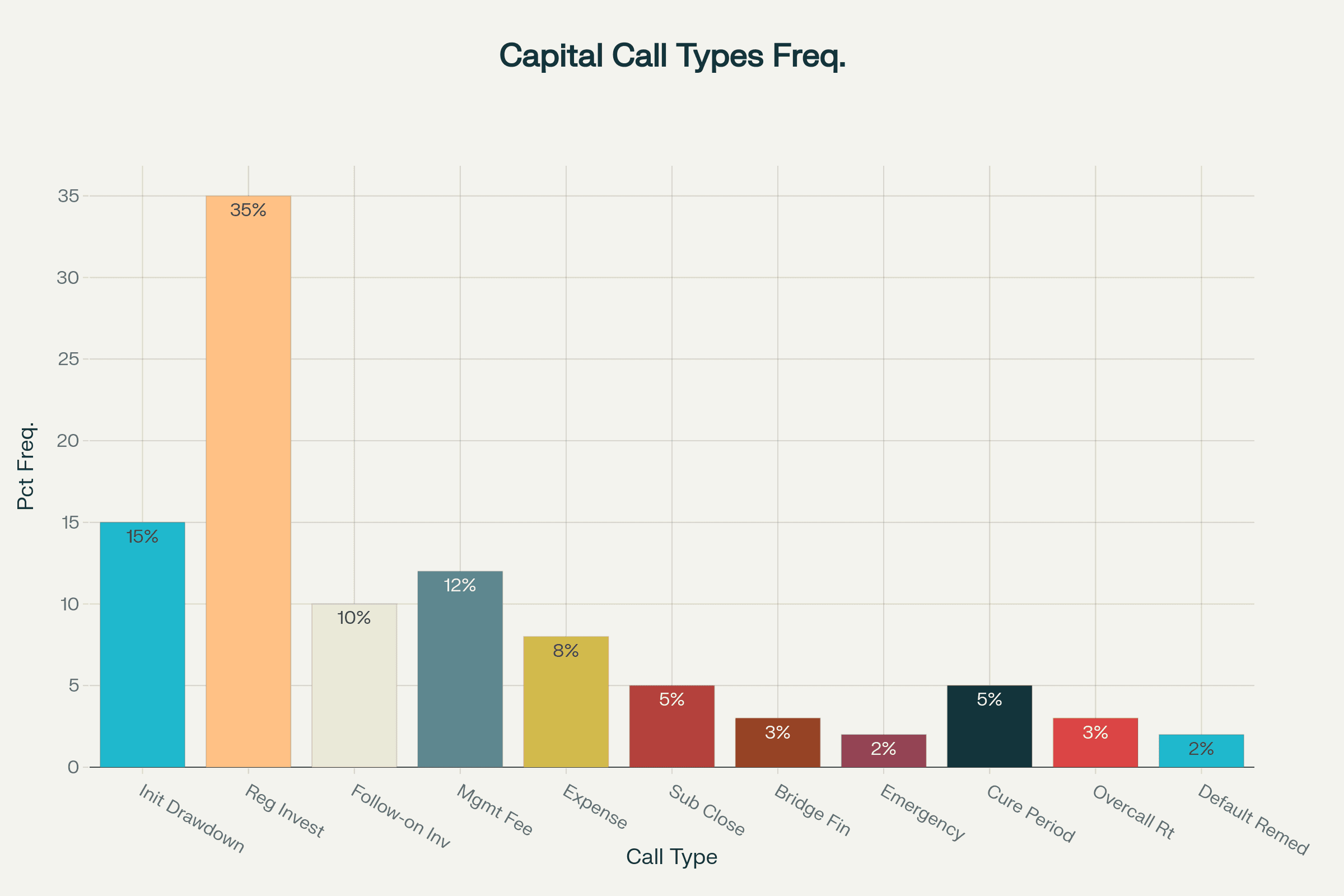

Capital calls serve various purposes throughout a fund's lifecycle:

Investment Capital Calls: The most common type, used to fund new portfolio investments or follow-on investments in existing portfolio companies. These typically represent 80-90% of total capital calls and may include provisions for broken deal expenses.

Management Fee Calls: Cover the fund's operational expenses and management fees, usually calculated as 2% of committed capital annually during the investment period, stepping down to a percentage of invested capital thereafter.

Expense Calls: Fund organizational expenses, due diligence costs, legal fees, and other operational needs not covered by management fees. Often subject to caps specified in the LPA.

Reserve Calls: Build reserves for future follow-on investments or to support struggling portfolio companies. GPs typically model reserve requirements at 10-30% of initial investments.

Equalisation Calls: Used when new LPs join at subsequent closings, these calls bring new investors to parity with existing LPs, including interest calculations on prior deployments.

Capital Calls vs. Committed Capital

Understanding the distinction between capital calls and committed capital is essential for both fund managers and investors. Committed capital represents the total amount an investor has legally pledged to invest in a fund over its lifetime. Capital calls, conversely, are the actual requests to transfer portions of that committed capital.

This structure creates several important dynamics:

For Fund Managers:

- Flexibility to time investments optimally without holding excess cash

- Reduced pressure to deploy capital immediately ("dry powder" management)

- Lower fund expenses (no need to manage large idle cash balances)

- Performance metrics (IRR) benefit from delayed capital deployment

- Ability to right-size fund commitments based on actual deal flow

For Limited Partners:

- Retained liquidity on uncalled capital with potential for interim returns

- Opportunity to earn returns on uncalled commitments through Treasury bills or money market funds

- Better cash flow management and reduced opportunity cost

- Ability to manage the "denominator effect" during market downturns

- Option to utilize subscription facilities for additional flexibility

The relationship between these concepts is governed by several key metrics:

- Paid-in Capital: The cumulative amount of capital calls that have been funded

- Unfunded Commitment: The remaining commitment available for future calls

- Call Percentage: The portion of total commitment being requested in a specific call

- Commitment Coverage Ratio: The ratio of liquid assets to unfunded commitments

- Overcall Amount: Potential calls above 100% of commitment (typically capped at 110-120%)

Timing and Frequency of Capital Calls

Capital call timing varies significantly based on fund strategy, market conditions, and deal flow dynamics:

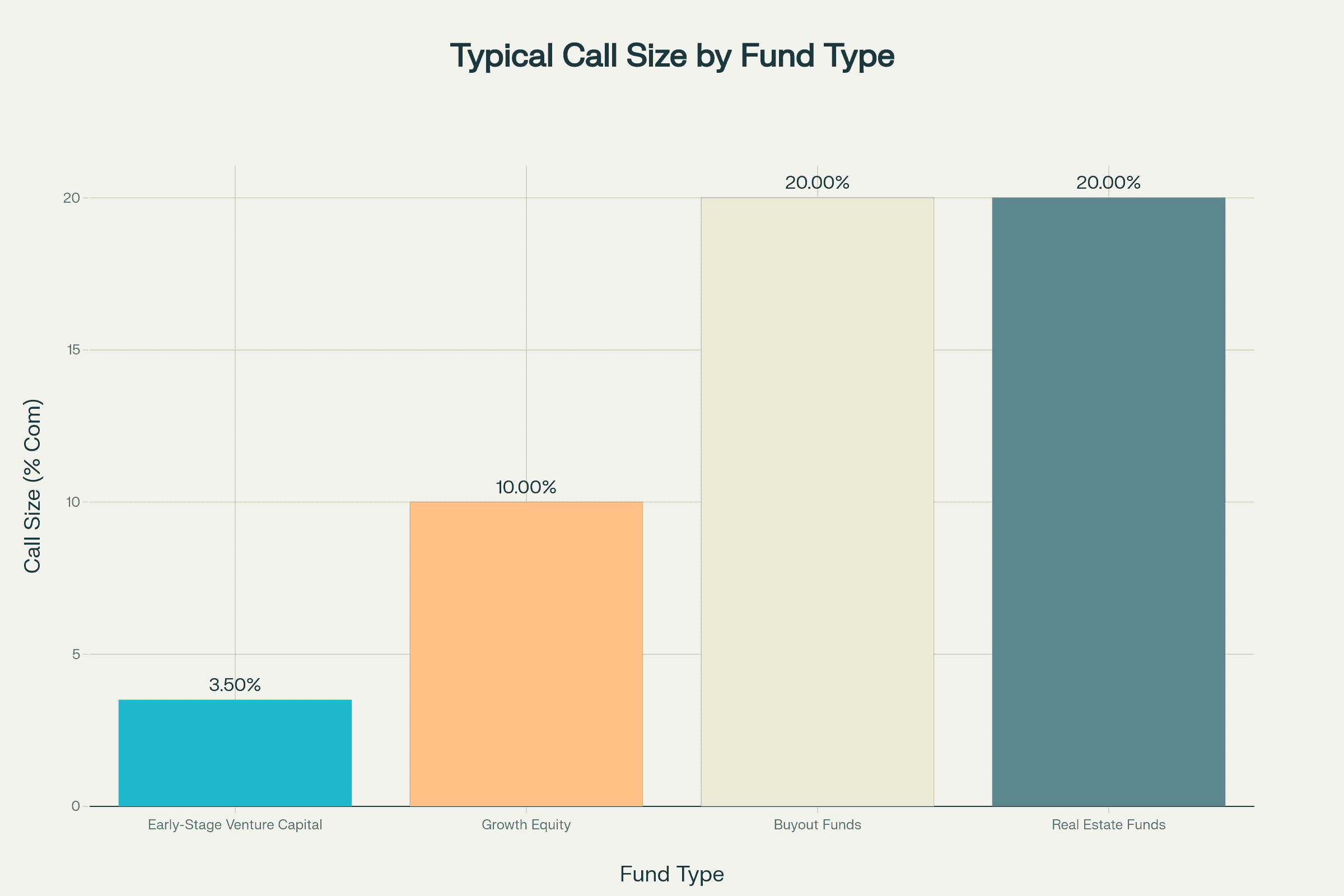

Early Stage Venture Capital: More frequent, smaller calls as funds make numerous seed and Series A investments. Calls might occur monthly or quarterly, each representing 2-5% of total commitment. The unpredictable nature of startup funding rounds requires LPs to maintain higher liquidity buffers.

Growth Equity: Moderate frequency with larger call amounts, typically quarterly, representing 5-15% per call as funds make fewer, larger investments. Calls often align with definitive purchase agreements.

Buyout Funds: Less frequent but larger calls, often semi-annually or deal-dependent, potentially calling 15-25% or more per occurrence for sizeable acquisitions. May utilize bridge financing more extensively.

Real Estate Funds: Highly variable based on deal flow and property acquisition timing, with calls ranging from 10-30% of commitment. Often tied to specific property closings with detailed use of proceeds.

Fund of Funds: Complex call schedules as they must manage inflows from their own LPs while meeting capital calls from underlying funds, requiring sophisticated cash management systems.

Legal Framework and Documentation

Capital calls operate within a strict legal framework established by the Limited Partnership Agreement (LPA) and related constitutional documents. Key provisions include:

Notice Requirements:

- Specific timeframes for advance notice (typically 10-30 business days)

- Acceptable delivery methods (email, registered mail, secure portals)

- Cure periods for addressing deficient notices

- Emergency call provisions for time-sensitive opportunities

Default Provisions: Consequences for failing to meet capital calls follow an escalating framework:

- Interest charges on late payments (often prime + 5-10% or 10-15% annually)

- Suspension of distribution rights and information rights

- Forced sale of partnership interest at significant discount (50-80% of value)

- Complete forfeiture of partnership interest and prior contributions

- Potential personal recourse in certain jurisdictions

Excuse Rights: Some LPs negotiate the right to be excused from specific investments due to:

- Regulatory conflicts (ERISA, Volcker Rule compliance)

- Tax considerations (UBTI exposure for tax-exempts)

- Policy restrictions (ESG exclusions, geographic limitations)

- Concentration limits specific to the LP's portfolio

Overcall Protections:

- Base commitment calls limited to 100% of original commitment

- Additional allowance for fees and expenses (typically 10-20%)

- Explicit caps on total callable amounts

- Requirements for LP consent beyond specified thresholds

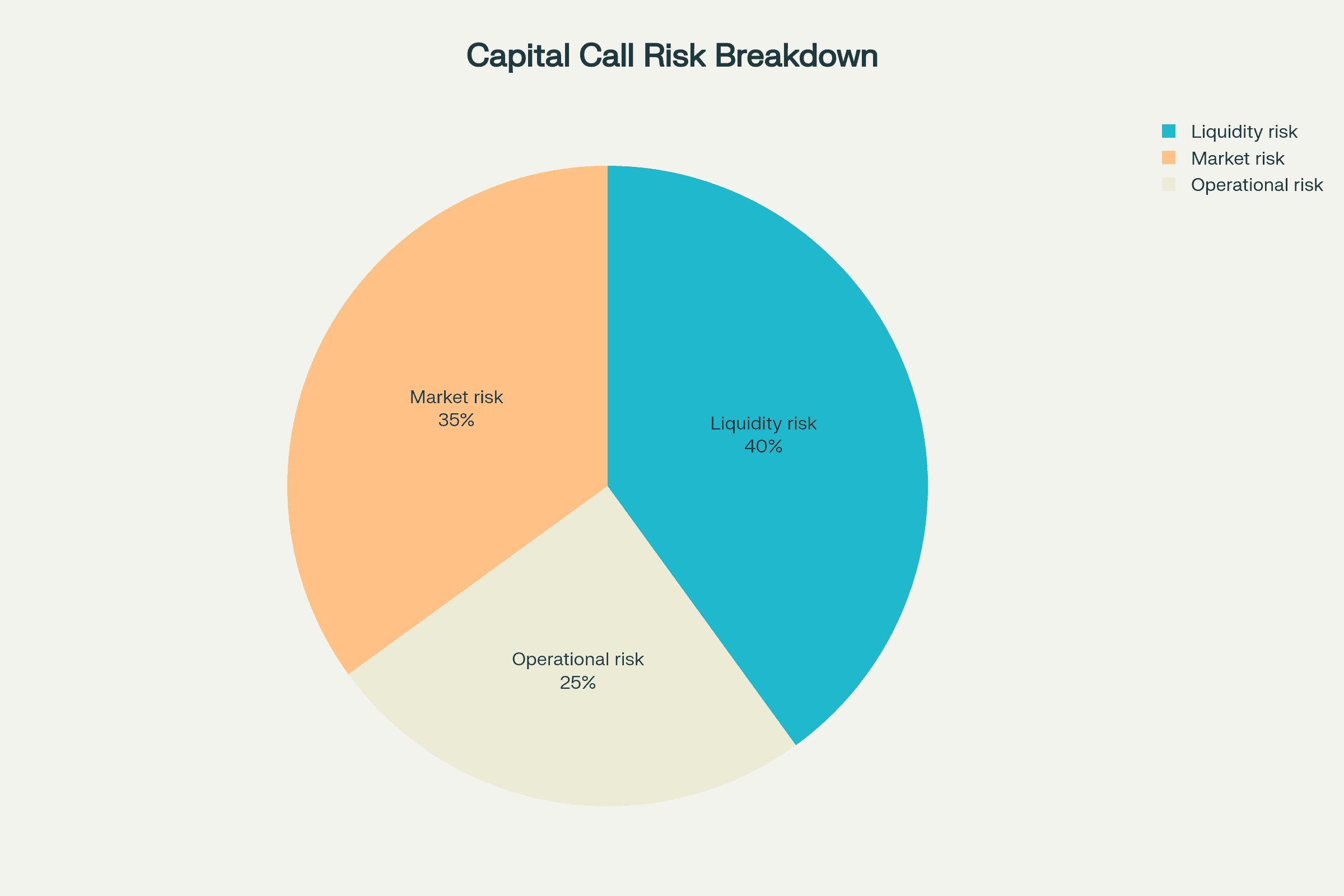

Managing Capital Call Risk

Both GPs and LPs must actively manage risks associated with capital calls through comprehensive frameworks:

For General Partners

LP Default Risk Management:

- Conduct thorough LP due diligence including creditworthiness assessment

- Diversify the LP base across geographies, types, and sizes

- Maintain standby credit facilities to bridge temporary funding gaps

- Include robust default provisions with teeth in the LPA

- Consider key person insurance for individual LPs

- Implement early warning systems through regular LP communication

Operational Risk Mitigation:

- Adopt ILPA-recommended templates and best practices

- Implement secure, automated fund administration platforms

- Maintain dual control processes for capital call approvals

- Regular testing of notice delivery systems

- Clear escalation procedures for time-sensitive calls

Timing and Liquidity Management:

- Develop dynamic cash flow forecasting models updated monthly

- Establish predictable capital call schedules where possible

- Consider LP liquidity cycles and known constraints

- Maintain regular pipeline communication with LPs

- Build buffer periods for large or complex transactions

For Limited Partners

Liquidity Risk Framework:

- Maintain minimum liquidity coverage of 1.5-2x near-term calls

- Utilize multi-tiered liquidity buckets with varying accessibility

- Implement stress testing for concurrent calls across portfolios

- Establish committed capital call facilities with relationship banks

- Monitor vintage year exposure and J-curve effects

Portfolio Management Strategies:

- Diversify commitment vintages to smooth cash flows

- Balance commitment pacing with distribution expectations

- Monitor and manage the denominator effect proactively

- Implement commitment budgeting aligned with strategic asset allocation

- Consider secondary sales for portfolio rebalancing if needed

Operational Excellence:

- Establish dedicated teams for capital call management

- Implement automated cash management systems

- Maintain comprehensive commitment tracking databases

- Regular reconciliation of fund records with internal systems

- Develop contingency plans for liquidity crunches

Capital Call Lines of Credit

Sophisticated LPs increasingly utilize capital call lines of credit (also called "subscription facilities") as a strategic liquidity management tool. These facilities have evolved from simple bridge financing to complex portfolio management instruments:

Structure and Terms

Facility Types:

- Committed Facilities: Banks obligated to fund with certainty of availability

- Uncommitted Facilities: Lower cost but no funding guarantee

- Hybrid Structures: Committed base with uncommitted accordion features

Pricing and Economics:

- Interest rates: SOFR/Term SOFR + 100-300 basis points

- Commitment fees: 15-50 basis points on undrawn amounts

- Arrangement and legal fees: $50,000-250,000 depending on complexity

- Financial covenants: Debt service coverage, portfolio concentration limits

Strategic Benefits

Portfolio Optimization:

- Remain fully invested in higher-returning assets until calls arrive

- Smooth cash flows across multiple fund commitments

- Potential IRR enhancement of 50-200 basis points through delayed funding

- Simplified treasury operations for complex portfolios

Risk Management:

- Reduce forced asset sales during market dislocations

- Maintain strategic asset allocation targets

- Provide buffer for unexpected large calls

- Enable opportunistic co-investments

Implementation Considerations

Governance Requirements:

- Board or investment committee approval for facility establishment

- Clear policies on usage limits and duration

- Regular monitoring of leverage metrics

- Integration with overall portfolio risk management

Operational Infrastructure:

- Robust systems for tracking facility usage

- Clear procedures for draw requests and repayments

- Regular mark-to-market of collateral coverage

- Coordination with fund administrators on capital calls

Best Practices for Capital Call Management

For Fund Managers

-

Communication Excellence:

- Provide detailed rationale for each capital call

- Offer informal advance notice for large calls

- Host periodic LP calls to discuss pipeline and capital needs

- Maintain transparency on fund pacing and deployment

-

Operational Robustness:

- Implement ILPA best practices for notice content and format

- Utilize secure, encrypted communication channels

- Maintain detailed audit trails for all capital movements

- Regular testing of capital call procedures

-

Relationship Management:

- Understand individual LP constraints and preferences

- Offer flexibility where possible within LPA parameters

- Proactive outreach for potentially challenging situations

- Regular face-to-face meetings with major LPs

-

Technology and Systems:

- Deploy institutional-grade fund administration platforms

- Automate routine calculations and allocations

- Integrate with LP portals for real-time information

- Implement robust cybersecurity measures

For Limited Partners

-

Strategic Planning:

- Develop comprehensive commitment pacing models

- Integrate capital call forecasting with broader portfolio planning

- Regular scenario analysis for stressed conditions

- Maintain strategic reserves for opportunistic investments

-

Operational Excellence:

- Dedicated teams with clear responsibilities

- Documented procedures for capital call processing

- Regular training on fraud prevention

- Integration with enterprise risk management

-

Relationship Building:

- Regular dialogue with GPs on liquidity position

- Participation in LPAC where offered

- Collaborative approach to solving timing issues

- Building reputation as reliable, sophisticated LP

-

Technology Infrastructure:

- Portfolio management systems with commitment tracking

- Automated cash flow forecasting tools

- Integration with treasury management systems

- Real-time dashboard for unfunded commitments

Common Questions About Capital Calls

What happens if I miss a capital call deadline? Missing a capital call deadline triggers the default provisions in the LPA, which typically follow an escalating series of remedies. Initially, you'll incur interest charges on the unpaid amount. Most funds provide a cure period (often 10-30 days) to remedy the default. If unresolved, consequences escalate to suspension of rights, potential forced sale of your interest at a significant discount, or complete forfeiture. The specific remedies depend on your LPA terms and the GP's discretion in enforcement.

Can I refuse a capital call? Generally, no. Capital calls are legally binding obligations under the LPA. However, some LPs negotiate "excuse rights" that allow them to opt out of specific investments conflicting with their investment policies or regulatory restrictions. Refusing a call without excuse rights constitutes a default with serious consequences including potential loss of your entire partnership interest.

How much notice do I get for capital calls? Standard notice periods range from 10-30 business days, as specified in the LPA. Many funds provide informal advance warning for large calls, and some LPs negotiate for extended notice periods (45-60 days) for calls exceeding certain thresholds. The notice period usually begins when the notice is sent, not when received, so LPs must maintain current contact information.

Are capital calls tax-deductible? Capital calls themselves are not tax-deductible as they represent equity investments that add to your tax basis in the partnership. However, the fund's activities may generate tax deductions or credits that flow through to LPs. Management fees and fund expenses may be deductible depending on the investor's tax situation, jurisdiction, and whether they qualify as investment expenses under applicable tax law.

Can capital calls exceed my original commitment? Most LPAs allow calls up to 110-120% of the original commitment to cover management fees, expenses, and other costs. This "overcall" provision should be clearly outlined in the fund documents. Any calls beyond the specified overcall percentage typically require explicit LP consent. LPs should factor this potential overcall into their liquidity planning.

How are capital calls calculated for new investors in subsequent closings? New investors joining at subsequent closings typically pay their pro rata share of prior investments plus an interest component (usually prime + 2-3%) to equalize their position with existing LPs. This ensures fairness as early investors have had capital deployed longer. The calculation includes all prior capital calls, fees, and sometimes a share of broken deal expenses.

What happens to defaulting LP interests? The treatment of defaulting LP interests varies by LPA but typically includes options for the GP to: sell the interest to other LPs at a discount, admit new LPs to assume the interest, retain the interest with modified economics, or distribute the defaulting LP's share pro rata among complying LPs. The remedies aim to ensure the fund can meet its investment commitments while penalizing the defaulting party.

Conclusion

Capital calls represent a fundamental mechanism in private equity and venture capital investing, balancing the liquidity needs of investors with the investment flexibility required by fund managers. The sophistication of capital call management has evolved significantly, with both GPs and LPs implementing institutional-grade processes, technologies, and risk management frameworks.

Success in this environment requires careful planning, clear communication, and robust systems to manage the competing demands of investment opportunity and investor liquidity. The rise of subscription credit facilities, automated fund administration platforms, and standardized best practices through organizations like ILPA have professionalized capital call management while introducing new complexities.

For fund managers, excellence in capital call management directly impacts fund performance, LP relationships, and ultimately fundraising success. For limited partners, sophisticated capital call management enables portfolio optimization, risk mitigation, and the ability to capture illiquidity premiums while maintaining overall portfolio balance.

As the alternative investment industry continues to mature, innovations in capital call structures, technology platforms, and liquidity solutions will further enhance the efficiency of capital deployment while strengthening the alignment between GPs and LPs. Whether you're a fund manager preparing to issue your first capital call or an institutional investor managing multiple fund commitments across vintages and strategies, mastering the capital call process is crucial for achieving optimal investment outcomes while maintaining strong, trust-based GP-LP relationships that endure across market cycles.